The maker of advanced humanoid and 4-legged robots (BigDog and Atlas), Boston Dynamics, is up for sale. According to the Financial Times, "this is one of those discordant moments that makes you question easy assumptions... and the current state of Alphabet and of robots."

Google acquired Boston Dynamics in late 2013 as part of Andy Rubin's 9-company shopping spree. At the time the company had 80 employes and many millions of dollars of research contracts from DARPA and the DoD. Although no financial information was provided at the time, various sources have estimated that Google paid $60 million plus extensive stock options. A more recent guesstimate from The Dallas Business Journal was $500 million.

Andy Rubin left the company in October 2014. After this the robot initiative was plagued by leadership changes, failed collaborations and an unsuccessful search for a new leader. Fomenting this lack of cohesion were Boston Dynamics executives who were reluctant to work with Google’s other robot engineers, according to a person familiar with the group.

The tensions spilled into recorded meetings and emails published on a Google worker forum. The documents were made available to Bloomberg News, which reported that Aaron Edsinger, director of robotics at Google in San Francisco, said he had been trying to create a low-cost electric quadruped robot with Boston Dynamics, but there was “a bit of a brick wall around the division.”

This recently released Boston Dynamics video of a humanoid robot trudging through the snow and being pushed over has been seen by almost 15 million viewers, but not enough to convince Google that it would generate real revenue. Consequently Alphabet, Google's parent company, has decided to sell Boston Dynamics "as it is not likely to produce a marketable product in the next few years," Bloomberg News reports, citing two people familiar with the plans. Possible buyers include Toyota’s research institute and Amazon, which makes robots for its fulfillment centers, according to the Bloomberg report.

Earlier this year The New York Times reported that "Google's robotics division has been plagued by low morale and a lack of leadership since the unit's founder left abruptly in 2014."

Alphabet, the new holding company that separated Google from its collection of speculative projects, has reframed the robots effort, moving it from a stand-alone division inside Google to a piece of the X research division. The company has also hired Hans Peter Brondmo, a technology industry veteran who last worked at Nokia, to help with management. X is using some element of robotics in numerous projects like self-driving cars; Project Wing, an effort to deliver packages with drone aircraft; and Makani, an effort to capture wind energy with high-flying kites.

This is also a moment for reality in robotics. The past two years have brought an unending stream of predictions about the coming “robo-calypse”. Just about the only thing left to discuss has been whether the robots will put us all out of work first, or whether a malignant AI will wipe us out.

As people working in the field are growing tired of explaining, the current state of the technology — though advancing fast — is a long way from these science fiction scare stories. The uncertain fate of Boston Dynamics underlines that truth. Even Google didn’t have the patience to wait for a walking robot to step out of the lab and earn itself a living.

3D Robotics is closing its San Diego facility, has reduced its staff at its Berkeley headquarters and in Austin, and acknowledged that co-founder and president Jordi Muñoz left the company at the end of 2015.

The latest staff reductions follow more extensive layoffs that took place at the end of 2015 after 3DR shifted its manufacturing operations from Tijuana to Shenzhen in order to economically mass produce their new Solo quadcopter which was intended to compete with DJI's Phantom line of quadcopters.

This is a consolidation we’ve been working on since before October of last year. As we shifted from the DIY era to consumer and to enterprise customers, we ended up with a different organization each time.

Anderson omitted talking about the problems 3DR faced with their Solo drone. The Solo started off with a flashy launch video that introduced the product about a year ago. DJI, at about the same time, released their new Phantom 3 with a list of features that surpassed the Solo. Because of producing and warehousing drones in China, 3DR made too many Solos particularly given how fast competitors were dropping prices and flooding the market. They built up a massive and costly inventory. A fully equipped Solo was priced too high for the market. 3DR was forced to lower prices to just $799 plus $199 for the gimbaedl platform, down from the initial price of $1,000 and $400. Keeping up the pressure, DJI cut its Phantom 3 prices ahead of its launch of the Phantom 4, a smarter and more sensor-laden drone all inclusively priced at $1,399.

In another interview with MarketWatch, Anderson said that 3DR was moving to the commercial market due to heavy competition in the consumer drone marketplace.

DJI is doing great, it’s because they are moving so fast, it’s forcing the others to adapt. Some companies are adapting by leaving, and others are adapting by moving upstream to the enterprise, which was always our plan. And [that move] is just accelerating right now.

3DR will now be focusing more narrowly on enterprise customers that are interested in using drones for such projects as utility line and pipeline inspections, and construction site inspections. As part of that move, 3DR announced the release of its Site Scan aerial analytics platform earlier this month. The technology enables corporate customers to conduct inspections and scan work sites with the Solo smart drone, and transmit the data to the cloud for processing and analytics. The system has a software-as-a-service monthly subscription model, which integrates Autodesk software, where using the 3DR Solo drone, businesses can upload aerial images, analytics and other data to the 3DR cloud. The system uses a tablet from Sony, a GoPro camera and starts at $3,249 for the hardware.

Anderson remains CEO, and Jeevan Kalanithi, 3DR’s chief product officer, becomes president. 3DR had ramped up to more than 350 employees but, with the current layoffs, will be down to below 80. The company’s former president, co-founder Jordi Muñoz, left the company last year as part of the ramping down of 3DR’s operations in San Diego and Tijuana.

"By making job cuts and refocusing, 3DR currently has enough financial runway until the second quarter of 2017 without having to go back to investors," Anderson said. “We want to make sure we have a good long year of runway,” he said. “You don’t want to have to go back to the market every six months. This is a moment when the investors want to see a profitable, lean operation, and we are doing that.”

iRobot has been streamlining its operations to focus on consumer products and enhancing shareholder value. Recent moves to divest their defense division, launch a low-cost Braava Jet floor cleaner, and investing in 6 River Systems all attest to their strategy.

Divested Defense Division

In a February transaction valued at $45 million, iRobot sold its Defense and Security division to Arlington Capital Partners. The divestiture ends iRobot's dual focus on the military and consumer markets and ends a multi-year revenue slide in the defense division. The sale was a strategically planned transition as the Iraq and Afghanistan wars wound down.

Colin Angle, iRobot Chairman and CEO, said: "In the spring of 2014, we engaged Blackstone Advisory Partners LP, now known as PJT Partners, to review strategic alternatives for our Defense and Security business. After a thorough and deliberate process, we've concluded the sale of the business to Arlington Capital Partners will maximize shareholder value by allowing us to focus on our much larger Home segment.

Launched New Low-priced Floor Cleaner

Earlier this month iRobot launched the Braava Jet Mopping Robot to add to their wet floor care business and to generate a new revenue stream beyond the Roomba line of vacuum products. The new robot is small -- about 6" square and 3" high -- with a nifty carrying handle -- and focused on cleaning hardwood floors and tight spaces by dry mopping, damp mopping (uses 60% of water compared to wet mode), and wet mopping. Each mode has a unique pad easily snapped onto the bottom of the robot (and snapped off over the trash bin) and identified by the robot as to which of the three functions it is to perform. The new little robot's best feature, however, is its low price: $199.

The Braava Jet is to be marketed heavily in China where the more expensive previous version of the Braava floor cleaner did quite well in year-over-year sales. In fact, according to CEO Colin Angle in an analysts financial call, said that growth in China was more than 70% year over year in 2015, driven primarily by the successful adoption of previous Braava models given predominately hard floor surfaces in the region. Hence the new lower-priced device is expected to be ideal in both the China and American markets.

Increasing Shareholder Value

In a recent letter to shareholders iRobot described its shift in focus toward the high-growth home robot business and by investing in projects that show the greatest promise for outsized returns.

iRobot is doing that with its existing and new products but also through its venture arm, iRobot Ventures, which just invested in 6 River Systems, a Boston-based startup of ex-Kiva executives developing fulfillment automation for e-commerce and retail operations. iRobot Ventures previously invested in Petnet, a smart feeder for cats and dogs, and Paracosm, a 3D vision and mapping technology company.

As an aside, Red Mountain Capital Partners, a VC which owns 6.1% of iRobot shares, and that invests in undervalued small cap companies and attempts to enhance and realize shareholder value through active ownership, is attempting to add two board members to the iRobot board at the upcoming stockholders meeting.

Throughout our nearly year-long engagement with iRobot, it has become clear that the Board will only take action in reaction to significant shareholder pressure. As such, we have nominated individuals who are highly qualified and would bring a much needed shareholder voice to the boardroom. Red Mountain has consistently called for improved Board oversight with respect to the Company’s allocation of capital, cost management, return on invested capital and corporate governance policies,” said Willem Mesdag, Managing Partner of Red Mountain.

In the letter to shareholders, iRobot does not recommend these two board members but another two of it's picking while citing that iRobot has delivered total shareholder return of 66% over the past three years compared to 59% for peers and 50% for S&P 500 companies.

Funding to robotics startup companies rose dramatically in 2015 reaching record highs in deals and dollars. CB Insights, a VC database provider, reported similar findings as seen in their quarterly financing chart.

Listed below are the results for March including two billion dollar acquisitions.

March Fundings:

6 River Systems raised $6 million in seed funding from VC firms Eclipse and iRobot Ventures. Founded in 2015 by former Kiva Systems and Mimio executives and based in Boston, 6 River is developing next-gen mobile robot fulfillment solutions for distribution centers.

SkySquirrel Technologies got $1 million in seed funding. The Halifax Nova Scotia startup is focusing on agricultural crop analytics.

nuTonomy, a spin out from MIT with offices in Singapore and Cambridge, received $3.6 million in seed funding in January for the development of autonomous vehicle technology to be initially tested in urban driving situations such as encountered by taxis.

Restoration Robotics, the robotic hair transplant company, got $4.82 million equity funding in January says Octa Finance, a Belize-based news company after researching Restoration's SEC filed Form D. CB Insights reported $7 million. So maybe there were other investors that will show up on later Form Ds.

Airware, the San Francisco UAS autopilot maker, got $30 million in a round that included former Cisco CEO John Chambers as an investor. Chambers will join the Airware board of directors.

Aarav Unmanned Systems, a spinoff from the Indian Institute of Technology Kanpur, received an unknown amount to enable the company to focus on GIS survey, precision agricultural and industrial inspections using UAS.

Aurora Flight Sciences, a Virginia-based developer of UAS tech for defense as well as commercial customers, has raised an undisclosed amount from Enlightenment Capital, a Chevy Chase, MD investor in aerospace companies. Earlier this month Aurora was awarded an $89 million contract for a vertical takeoff and landing X-plane for the DoD.

March Acquisitions:

ThermoFisher Scientific is acquiring Affymetrix for $1.3 billion. Adding Affymetrix's products will help ThermoFisher expand its array of lab equipment and robots into biosciences and genetic analysis workflows.

General Motors acquired Cruise Automation, a startup that develops autopilot systems for existing cars, for an undisclosed sum but, according to Fortune magazine, a figure "north of $1 billion."

Pasco Scientific, a provider of educational robots, acquired Ergopedia, the maker of the ErgoBot educational bot, for an undisclosed amount.

PCS Edventures, a provider of STEM, robotic and UAS educational tools and programs, acquired the assets, IP and inventory of Thrust UAV, an Idaho startup, for $109,000. Shortly thereafter Thrust, a service provider with a racing drone, announced an $825,000 contract to provide their drones to a reseller.

The robotics industry has graduated to be big business -- at least for research firms. 47 different reports on subjects ranging from broad to very drilled-down views of the industry are analyzed and projected upon with widely differing forecasts.

Below are short profiles of each of those 47 reports. Many of the reports duplicate the coverage of others and frequently differ on forecasts. Some are marginally useful; others are chock full of valuable information. But bottom line, all the reports are forecasting positive double-digit growth for most segments of the robotics industry.

INDUSTRIAL ROBOTICS (13)

Global industrial robots, Dec 2015, 113 pages, Grade Market Data, $1,200

The report forecasts that the number of industrial robots in use will increase from 1.658 million units in 2015 to a new peak of 2.96 million by 2020.

Global industrial robotics, Jan 2016, 129 pages, Hoovers Research, $3,850

Forecasts their take on the top 18 robotic companies for the period 2016 to 2022.

Global industrial robotics in heavy industries, Feb 2016, 46 pages, TechNavio, $2,500

Forecasts the market for industrial robotics in heavy industries to grow at a CAGR of 6% during the period 2016-2020.

Global automotive robotics, Nov 2015, 167 pages, BIS Research, $3,395

Forecasts a "dynamic era of growth due to the rising demand for vehicles of all types."

Global articulated robots, Dec 2015, 123 pages, TechNavio, $2,500

Forecasts this subset to grow at a CAGR of 16.27 over the period 2015-2020.

Global assembly-line robots, Dec 2015, 54 pages, TechNavio, $2,500

Predicts these robots to grow steadily at a CAGR of 7% through 2020.

Industrial robots in China, Mar 2016, 60 pages, China Research & Intelligence, $2,400

Forecasts that CAGR of annual installation of China's industrial robots will surpass 20% during the period to 2020.

Robot industry in China, Mar 2016, 131 pages, QY Research, $3,200

The report focuses on China major leading industry players providing information such as company profiles, product picture and specification, capacity, production, price, cost, revenue and contact information.

Global welding robots market, Sep 2015, 69 pages, TechNavio, $2,500

Forecasts this segment to grow at a CAGR of 6.09% through 2019.

Global and Chinese robotic welding systems, Jan 2016, 150 pages, Prof Research

This report explores Chinese vendors in detail and presents capacity, production value, and 2011-2016 market shares for each company.

Industrial robots in food and beverage, Nov 2015, 167 pages, TechNavio, $2,500

Global industrial robotics used in the food and beverage industry to multiply at a CAGR of close to 29% during the forecast period.

Material handling robots, Nov 2015, 61 pages, TechNavio, $2,500

The global material handling robotics market to grow at a significant rate of nearly 9% and exceeding $20 billion by 2019.

Cartesian/Gantry/Rectilinear industrial robots, Feb 2016, 124 pages, Grace Market Data, $2,000

The use of Cartesian robots, ofen used as a CNC machine or for milling or drawing, is growing and this report expects that growth to continue through 2021.

MOBILE ROBOTS & UNMANNED AIR, LAND AND SEA VEHICLES (15)

Global agriculture robotics, Nov 2015, 171 pages, Global Industry Analysts $4,500 Focuses on unit shipments by 46 profiled companies covering weeding, harvesting, UAS, driverless systems, crop scouting, greenhouse operations, livestock farming and milking robots.

Global AGV industry, Mar 2016, 125 pages, Research in China, $2,400

Reports that units in 2015 were up 35% from 2014 and that 27% of global total was in China, up 36% from 2014.

Global drones market, Mar 2016, 55 pages, Daedal Research, $800

Profiles key players 3D Robotics, AeroVironment and DJI.

Global drones market, Mar 2016, 1,114 pages, Wintergreen Research, $4,100

Forecasts the worldwide market at $6.8 bn in 2015 to $36.9 bn by 2022.

Global UAV market, Jan 2016, 67 pages, TechNavio, $2,500

Forecasts the global UAV market to grow at a CAGR of 10.16% during the period 2016 to 2020.

Global UAV market analysis, Feb 2016, 200 pages, BIS Research, $3,999

Forecasts that the commercial drones marketplace will have exponential growth in the next 5 years.

Global defense drones, Dec 2015, 46 pages, TechNavio, $2,000

Defense drones market forecast to grow at a CAGR of 6% through 2020.

Global civil and military UAV industry, Oct 2015, 112 pages, Lucintel, $3,900

Forecasts the combined UAV industry to grow at a CAGR of 7.1% from 2015 to 2020.

Global small UAV market, Jan 2016, 72 pages, TechNavio, $2,500

Forecasts growth at a CAGR of 6.52% during the period 2015-2020.

Unmanned underwater vehicles market, Mar 2016, 255 pages, Markets and Markets, $4,650

The global market for UUV, ROV and AUV is projected to grow from $2.29bn in 2015 to $4bn by 2020 at a CAGR of 11.9%.

Global aerial imaging market, Mar 2016, 52 pages, TechNavio, $2,500

Forecasts the global aerial imaging market to grow at a CAGR of 13.28% during the period 2016-2020 as the transition from high-cost piloted aircraft takes place.

Global unmanned ground vehicles market, Sep 2015, 123 pages, Markets and Markets, $4,650

The global UGV market is projected to grow from $6.4 billion in 2015 to $18.6 billion by 2020.

Global unmanned sea systems, Dec 2015, 55 pages, TechNavio $2,500

Forecasts market growth of 6% CAGR during the period from 2016 to 2020.

Global oil & gas drones, Feb 2016, 129 pages, Hoovers Research, $3,850

This report analyzes market dynamics such as drivers, constraints, opportunities, threats and challenges.

North American oil & gas drones, Jan 2016, Mordor Intelligence, $3,465

Forecasts this market segment to grow at a 40.7% CAGR to 2020.

HEALTHCARE SERVICE ROBOTICS (8)

Prosthetic and therapeutic robotics, Dec 2015, Lux Research

The prosthetic and therapeutic robotic devices sector will grow into a $1.9 billion and $1.7 billion market by 2025 respectively.

Exoskeleton robots, Feb 2016, 49 pages, TechNavio, $2,500

Forecasts the global exoskeleton robots market to grow at a CAGR of 50.85% during the period 2016-2020.

Rehab robots, Jan 2016, TechNavio, 47 pages, $2,000

Forecasts the global rehabilitation robots market to grow at a CAGR of 24.51% during the period 2016-2020.

Hip and knee orthopedic surgical robots, Jan 2016, 145 pages, Wintergreen Research $4,100

This market segment was only $84 million in 2015 but is forecast to reach $4.6 billion by 2022.

Spine surgical robots, Feb 2016, 313 pages, Wintergreen Research, $4,100

This market segment is forecast to reach $2.7 billion by 2022.

Abdominal surgical robots, Dec 2015, 416 pages, Wintergreen Research, $3,900

Worldwide market valued at $2.2 billion in 2012 and forecast to grow to more than $10 billion by 2021.

Radiology oncology surgical robots, Jan 2016, 557 pages, Wintergreen Research $4,100

This market segment is expected to reach $7.3 billion by 2022.

Global robotic vacuum cleaner market, Feb 2016, 51 pages, TechNavio, $2,500

Robotic vacuum cleaner market will grow at a CAGR of 15.3% and reach $3.31 billion by 2020.

Robotic lawnmower market, Jan 2016, 175 pages, Beige Market Intelligence, $2,995

Forecasts robotic lawnmower market to hit $2 billion by 2021.

Global telepresence robot market, Mar 2016, 482 pages, Wintergreen Research, $4,100

Telepresence robots at $825 million in 2015 are forecast to reach $7 billion by 2022.

Smart robots market, Mar 2016, Transparency Market Research, $4,315

Analyzes key players including iRobot, Honda Motors, Adept Technology, Lely Group, Google, Amazon, Northrop Grumman, Bluefin Robotics, ABB and Yaskawa Electric.

ANCILLARY BUSINESSES (4)

Global LiDAR market, Mar 2016, 145 pages, Markets and Markets, $5,650

LiDAR and low-cost variants are expected to grow at a CAGR of 12.4% and reach $3.22 billion by 2022.

3D machine vision market, Nov 2015, 151 pages, Markets and Markets, $4,650

This market segment is expected to hit $1.63 billion by 2020 growing at an estimated 10.5% CAGR.

Robotic vision market, Mar 2016, 195 pages, Markets and Markets, $4,650

This segment expected to grow at 10.8% from 2015 to 2020.

Global UAV payload market, Dec 2015, 112 pages, Strategic Defense Intelligence, $4,800

Radar, comms, sensors, cameras, gimbal devices all make up the "payload" market which was $2.1 bn in 2015 and is expected to reach $3.2 bn by 2025. Only 3.93% CAGR which reflects both fast growth and costs continuing to drop.

FINALLY (2)

The fact-based backbone for many of these research reports is the International Federation of Robotics (IFR) annual World Robotics Industrialand World Robotics Service reports. These two books represent the official tabulation from all the robot associations around the globe. The 2015 reports cover 2014 activity. The two 2015 reports can be purchased for $2,275. The IFR industrial robots report forecasts a 15% CAGR (compounded annual growth rate) for the next 4 years and, for the same period, the service robots report forecasts a 19% CAGR for professional and field service robots and 27% CAGR for household, consumer and personal service robots. Reports covering 2015 will be published this summer.

In March 2012, in an effort to make their distribution centers (DCs) as efficient as possible, Amazon acquired Kiva Systems for $775 million and almost immediately took them in house.

There was confusion after the acquisition whether Kiva would continue providing DCs with Kiva robots. Although Kiva said that they would continue selling their technology to other retailers it soon became clear that Amazon was taking all Kiva’s production and that, at some future date, Kiva would stop supporting their existing client base and focus entirely on Amazon – which happened in April 2015 when Amazon renamed Kiva to Amazon Robotics and encouraged prospective users of Kiva technology to let Amazon Robotics and Amazon Services provide fulfillment within Amazon warehouses using Amazon robots.

Consequently, there has been a scramble of new providers to fill the void left by Kiva’s technology, warehouse software systems and robots being removed from the marketplace. Many of these startups were showing their robotic systems at MODEX 2016 held at the Georgia World Congress Center in Atlanta. MODEX is a big material handling equipment, technology and systems show with 850 exhibitors, 250,000 sq ft (23,225 sq mt) of expo space, 100 informational seminars and over 25,000 attendees.

Kiva’s robots and inventory management system were breakthrough technologies in 2011 and 2012 enabling items that were to be shipped to be brought to the packer near the truck door, instead of the more traditional method of the picker/packer going out into the warehouse, picking the goods, and returning to pack and ship them. At the time Kiva started operations, robotic picking was still a premature science. Consequently Kiva focused on managing the rest of the process: receiving, de-palletizing and storing items and bringing dynamically-stored shelves containing ordered items to the picker/packer to pick, pack and ship while the Kiva robot returned the shelves to the most appropriate area in a free-form dynamic warehouse and autonomously went off to bring the next shelf to another picker/packer.

Although vision systems and grasping technologies have improved since then, they still aren’t fast and flexible enough to replace humans so, instead, most new systems attempt to augment humans by reducing what they have to carry and the distances they have to travel to get the items that were ordered.

Source: Locus robotics

Fulfillment systems

Iam Robotics, a Pittsburgh startup founded by a couple of CMU grads, is the only vendor that uses a robot arm to grip goods. It 3D scans and identifies items to be picked into a cloud library and then uses a mobile picking robot to go to and pick items, place them in a tote, and then place the completed tote on the nearest conveyor to a packing station.

Locus Robotics, a Massachusetts-based company founded specifically in answer to the Kiva situation by a Kiva-using DC owner, uses a fleet of robots integrated into current warehouse management systems to provide robotic platforms to carry picked items to a conveyor or to the packing station thereby reducing human walking distances and improving overall picking efficiencies.

6 River Systems, a Massachusetts startup comprised of ex-Kiva execs, had a booth but wasn’t even showing a photo of their solution. VCs have seen the 6 River System, however, and value it highly: 6 River just got $6 million in financing from a group of VCs including iRobot.

Fetch Robotics, a Silicon Valley startup that uses two different robots: one to pick and the other to assist workers as they pick by carrying the items and taking completed orders to the shipping station – autonomously.

Magazino, a German startup that was not at MODEX, has a mobile picking system that has a retractable and rotatable column with a gripper system and a removable shelf. It is able to grasp rectangular objects from small softcovers to shoeboxes up to heavy cases. The robot stores items in its built-in shelf and delivers it to a shipping station.

Grey Orange, an Indian startup that was also not at MODEX, has a system and product line strikingly similar to Kiva’s original offerings except that their robot is square and Kiva’s is round. GreyOrange has over 300 employees and its robots provide service to India’s e-commerce giants Flipkart, Jabong and Mahindra and has been signing distribution partners in Japan and throughout Asia and the Pacific.

InVia Robotics, also not at MODEX, a Southern California startup with two robots very similar to Fetch Robotics’ except InVia’s method of picking is similar to Magazino’s. It grabs items and slides them onto a platform which then slides the item into a bin and, when the order is complete, slides it onto an autonomous mobile delivery robot.

Mobile platform systems

Mobile platform systems are designed to work across multiple environments – DCs, warehouses, factories – and are autonomous mobile platforms that can be fitted with special-purpose payloads such as for receiving, restocking, inventory, moving material from work cell to work cell, picking, supporting human pickers, packing and palletizing. Many vendors have provided AGVs, carts, lifts and tows, and have done so for many years. The older versions of these systems use markings, tapes, beacons, sensors and other things on the floors and ceilings to provide location information. Newer systems use the latest 3D vision systems, collision avoidance and mapping software to easily enable autonomous point-to-point navigation.

Clearpath Robotics is offering 2 transporters: one for heavy loads of up to 3,300lbs and the other for light loads of up to 220lbs. Both can be fitted with a carrying cart, bin carrier or a plain flat plate, and both have an intuitive lighting system similar to white headlights in the front, red in the rear. Clearpath is an established provider of robotic utility vehicles for the military and academia and are taking that experience to provide solid mobility platforms for customers to do their own thing.

MiR Mobile Industrial Robots, a Danish startup headed by Thomas Visti (who was VP at Universal Robots of collaborative robots fame), has begun to sell a small transport for logistics and healthcare. It operates as both a tug and/or a platform. It has 2 scanners and a 3D camera to make sure that it sees people and obstacles.

Next-gen AGVs: Vision guided robots

Seegrid calls today’s vision guided vehicles the next generation of AGVs. Many vendors have, for years, provided material handling AGVs used to tow carts and pallets around warehouses, hospitals and factories. They depend upon beacons or floor and wall markings for their navigation and are efficient but klutzy.

Erik Nieves, who previously headed US Yaskawa Motoman and is now in stealth mode with his startup Plus One Robotics, said:

“Perfecting perception and grasping have been major holdups – particularly for the applications that most factory and warehouse executives crave: autonomously loading and unloading trucks and containers, and ‘each picking’ (the automated means to handle and package goods). The development of these technologies has been hindered by the acquisition of Industrial Perception (IPI) by Google in 2013. IPI was at the forefront of clever AI combined with ranging sensors and cameras in being able to quickly identify, categorize and instruct the robot how best to grasp random objects. Since their acquisition, their technology is no longer visible to the market.”

Armed with lower-cost LiDARs and Kinnect-like infrared 3D camera systems, new players like Aethon and Seegrid entered the market with new capabilities – including being able to autonomously unload containers: vision guided robotic lifts, tugs and platforms.

Aethon is a Pittsburgh-based provider of autonomous tugs used in hospitals and factories. Some of their AGVs (they have more than 400 in the field) have been outfitted for secure medication delivery, and all of their robots are assisted with their Cloud Command Center, a 24/7/365 remote monitoring service to get the tug out of whatever unplanned situation in which it finds itself.

Seegrid, also based in Pittsburgh, has focused their vision guided kits and lifts on the distribution center marketplace (their main investor/partner is Giant Eagle, a large East Coast grocery chain supported by multiple distribution centers). Seegrid has also partnered with forklift manufacturer Raymond to integrate their vision guided system onto Raymond lifts. Most recently Seegrid unveiled a monitoring system likened to a subway platform display showing when the next train is coming, to provide awareness to approaching devices and also to provide human assistance when needed.

Balyo, a French manufacturer of handling robots has recently partnered with Linde and Hyster Yale to integrate and provide their vision guided systems onto forklifts and tows manufacturered by Linde and Yale.

As an aside, Seegrid recently held a contest to acknowledge journalists covering the materials handling industry and they awarded The Robot Report third place at an Awards Celebration event held after hours at MODEX in Atlanta. First place went to John Hitch, a staff writer at New Equipment Digest; second place went to Bob Trebilcock, Exec Editor at Modern Materials Handling. Thanks very much.

If you enjoyed this article, you may also want to read:

Dmitry Grishin at the Skolkovo Robotics conference in Russia.

In 2012, Dmitry Grishin, co-founder and CEO of Mail.Ru Group, the largest Internet and social networking company in the Russian-speaking world, seeded a fund with $25 million of his own money to focus on robotic startups.

This month Grishin Robotics launched another fund with $100 million provided by institutional and individual investors from Europe and the U.S. to focus on companies involved in the “Hardware Revolution.”

“Until recently, people mainly thought about robots as multi-functional products in humanoid form-factor. Today single-purpose devices, combining sensors with software and data analytics components, have the potential to radically automate the physical world around us — eliminating “dirty, dull & dangerous” tasks from our lives and, thus, realizing the ultimate purpose of robotics. The investment focus of the new fund reflects this vision, as Grishin Robotics looks to fund both hardware & software companies, driven by the six pillars of the Hardware Revolution — (1) cheaper components, (2) ubiquitous connectivity, (3) smartphone penetration, (4) 3D printing, (5) disruption of supply chain and (6) crowdfunding. By 2020, total value of the markets driven by these changes, is estimated to reach $1 trillion.”

The new fund will be primarily focused on Series A & B deals, with a certain amount of capital reserved for seed and later-stage opportunities — such as Ring, a web-based video doorbell consumer product, whose Series C round was the first investment from the new fund. Grishin Robotics is looking to expand its B2B focus as well as B2C, and will allocate up to $10 million over the lifecycle of portfolio startup companies.

Auris Surgical Robotics will acquire Hansen Medical for $80M+, PrecisionHawk raised $18M to help bring commercial drones safely into US airspace, and SkySafe raised $3M to disable badly behaving drones in the very same airspace.

PrecisionHawk Inc. has raised $18 million in a Series C round of funding from Verizon Ventures, USAA, NTT Docomo Ventures and Yamaha Ventures. The money will be used to help companies use drones for various commercial purposes in US airspace, without getting into areas where they can’t fly safely or legally. PrecisionHawk had been known as the maker of the Lancaster fixed-wing drone for farmers — gathering aerial data about land and crops and using a variety of cameras and sensors.

CEO Bob Young said, “Building and selling planes will arguably be the smallest part of our business. Our biggest opportunity and the faster growing part of our business is the platform we built for aerial data services.”

SkySafe got $3M from Andreessen Horowitz, Founder Collective and SV Angel, to disable badly behaving drones. SkySafe, is a six-month-old, San Diego-based provider of technology that can disable drones that are flying where they shouldn’t.

AirMap, a Santa Monica, CA provider of airspace information for airports and drone operators, just a few days earlier got $15M for a Series A funding led by General Catalyst Partners. AirMap focuses exclusively on providing accurate airspace information so that others in the industry can focus on building drones, collision avoidance AI, payloads, and applications.

Auris Surgical Robotics, Inc. and Hansen Medical, Inc. today announced that they have signed a definitive merger agreement under which Auris will acquire Hansen Medical for $80 million in cash. In addition, certain significant stockholders of Hansen Medical have agreed to invest approximately $49 million into Auris with the closing of the transaction.

“Hansen Medical has developed a technology leadership position in the field of intravascular robotics,” commented Dr. Fred Moll, Chief Executive Officer of Auris. “There remains a significant opportunity in flexible robotics and I am excited to combine with Hansen Medical to advance this market.”

“We are pleased with this outcome. The combined capabilities of Auris and Hansen Medical will accelerate the proliferation of medical robotics to advance patient care,” said Cary Vance, President and CEO of Hansen Medical.

Paslin, a Michigan integrator of welding robots, automation systems, and tooling, was acquired by Wanfeng Technology Group for an undisclosed amount (but reported as $302 million in China Daily).

PASLIN

Established in 1937, Paslin is an integrator of robot welding and assembly systems and is a full-service design and build organization serving the automotive industry. Paslin also provides special welding and resistance spot welding equipment, and provides engineered automation system solutions. Paslin employs 700 and has derives most of its sales from customers in the US and Canada.

WANFENG

Founded in 1994, the Wanfeng group of companies, located 125 miles southeast of Shanghai, is mainly known for their auto wheels and aftermarket wheels and auto parts. But it also has businesses in such fields as robot integration of assembly, welding and painting systems, automation equipment, magnesium alloy parts, aviation equipment and financial investments, with annual sales of $3 billion.

Wu Jinhua, Wanfeng's chairman and CEO, said: "Paslin has accumulated advanced technologies and client groups in the field of automated welding in North America, and this acquisition could not only help Paslin realize its globalization, but also enhance Wanfeng's competitiveness in industrial robot system integration technology. This acquisition is a win-win situation."

According to Forbes, besides Zhejiang Wanfeng Auto Wheel, whose customers include Yamaha, the Wu clan controls Shenzhen-listed Zhejiang RIFA Precision Machinery, a supplier of grinding, boring and other machines.

CHINA'S GROWING ROBOT ARMY

In a recent story in the Financial Times, Asia-focused asset management firm Mirae Asset Management forecasts that China's robot army will expand at a compound annual growth rate (CAGR) of 35% until 2020.

Rahul Chadha, chief investment officer of Mirae, says: “Using the rule thumb that one industrial robot replaces four to five workers, this suggests that robots have rendered more than 1m people jobless.” Mr Chadha, who calculates that robots will replace around 3.5m Chinese workers over the next five years, says: “The message that comes from the leadership is on improving productivity via automation. They are paranoid about doing things quickly. They believe they have got to because their competitors will do the same."

THE ACQUISITION MARKETPLACE

Siasun Robot & Automation, China's most prominent robot manufacturer, announced that they are planning to acquire competitive and domestic international component manufacturers to expand their market presence.

“We have been in negotiations with potential companies for over a year and we hope to complete these acquisitions by June,” Vice Chairman and President Qu Daokui told ChinaDaily.com.

At present, more than two-thirds of the robots purchased in China are produced by international vendors but that ratio is rapidly changing. The most recent Chinese National 5-year plan calls for increased use of robots and local governments are supporting the effort with various real estate and tax incentives. Many "deals" have been arranged whereby Chinese venture funds are investing in robotic ventures from Russia, Israel, Silicon Valley and through acquisitions such as the Ninebot acquisition of Segway last year, the current Paslin acquisition and Siasun's ambitious plans.

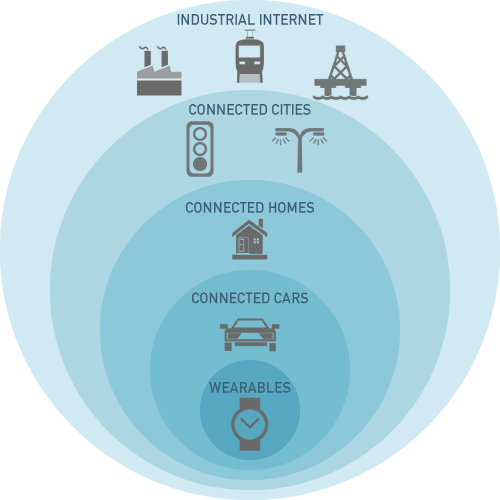

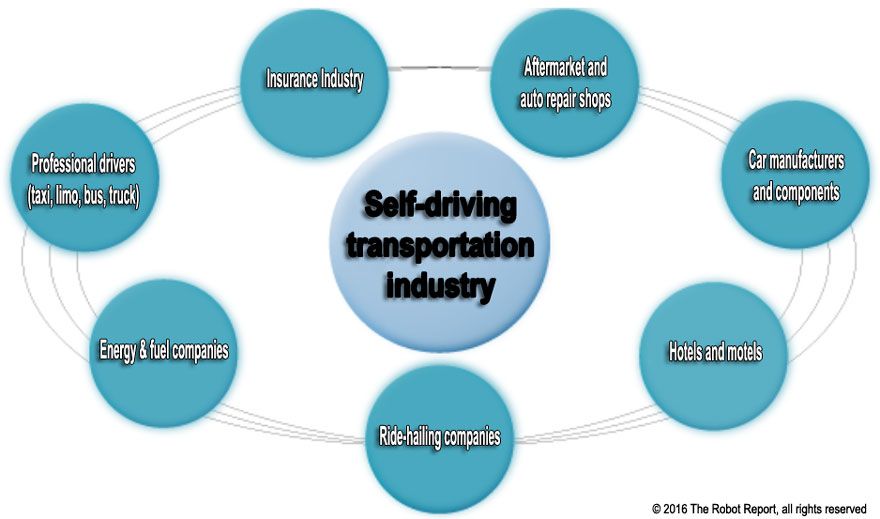

Volumes have been written about the possible beneficial (and negative) effects of self-driving cars and systems. But few have studied what industries will be disrupted by the transformations as self-driving devices begin to provide for our transportation needs.

The stakeholders are numerous and the effects can be devastating. Think secretaries, airline reservation agents, and others disrupted during the emergence of the digital era. The transition to self-driving vehicles and car-sharing systems is likely to cause similar worldwide disruptions. Self-driving vehicles are penetrating a wide variety of industries – from factories to warehouses to underwater and into the skies. For the purposes of this article, the focus will be on cars, trucks, and public transport.

Consider the insurance industry. If accident rates go down by 90%, as many are predicting, premiums will need to go down too because the reserves for payouts, which are built into the rates, will go down as well. Also, there will likely be fewer insured drivers and car owners thereby lowering the pool of insured people.

Consider hotels and motels and their real estate values and employees – particularly those along the major highways. Why stop at a motel when you can sleep comfortably in a long-haul driverless car? This will likely effect short-haul airlines and airline employees as well.

Think about professional drivers – truckers, taxies, limos, buses, shuttles. It is expected that many will be replaced by on-demand point-to-point self-driving devices. The list goes on and on.

Source: The Robot Report

CB Insights, a venture capital database and research firm, highlighted 14 industries that are likely to be seriously disrupted as self-driving cars hit the marketplace:

Insurance companies – as demand for insurance goes down as risks of crashes drop, insurance companies will lose revenue from this segment of their business.

Auto repair companies – fewer accidents will mean fewer trips to the repair shop.

Professional drivers (taxi, limo, trucking) – as demand for drivers gets reduced, there will still be a need for more highly skilled drivers and fleet managers.

Hotels and motels – drivers will be able to sleep in comfortable long-distance cars as they zip along the highways.

Domestic and short-haul airlines – many people will choose to take a comfortable car ride instead of going through the many hassles of air travel.

Aftermarket and auto parts – as smart driving and assistance software and systems get deployed, there will not only be fewer accidents but less need for replacement parts and aftermarket upgrades.

Ride-hailing companies – will Uber and the others be able to make the transition to owning their cars and managing the ownership aspect of fleet management? Or will the car companies fill this need like GM is planning to do with their deal with Lyft to combine GM’s fleet production and management with Lyft’s point-to-point service?

Public transportation and rental cars – buses have fixed drop-off points whereas ride-hailing companies can go point to point. Why walk that extra distance? And why rent a car when you can just as easily call for a self-driving vehicle?

Parking garages, lots and street spaces – long-term parking will descrease as car fleets are continuously on the move. Reshaping street spaces remains to be imagined.

Fast food companies – at present, 70% of McDonald’s US revenue comes through the drive-thru window, thus they and other fast food companies, particularly those near highway exits, will take a big hit.

Energy & petroleum companies – although the mix of energy used to fuel self-driving cars may shift to electricity, researchers are predicting that the driverless car era will actually consume more energy.

Real estate – fewer gas stations and garages may just be the tip of the iceberg. Since commuting will be faster and easier, residential property value will shift from urban to suburban areas.

Media & entertainment – concept self-driving cars, like the Mercedes one shown above, will have screens for people to watch movies, read and see the news, and provide a more relevant time spent commuting.

Car manufacturers – although there’s time for car companies to adapt to the new reality of self-driving devices, many serious and disruptive changes are likely to happen: fewer consumers will own cars, and, although Uber and the others will have bigger fleets with corresponding fleet economic efficiencies, the overall number of cars produced will go down as car-sharing increases utilization.

Of course, there are those who argue that this level of disruption won’t happen – that we won’t ever fully adopt self-driving vehicles. These naysayers provide a list of present-day facts that will need changing before self driving cars will make a significant dent in the kind of stakeholder changes described above:

A lot of people like to drive

A lot of people live in areas with low population density, where car sharing will be impractical

A lot of people have kids, pets, a big family, disabilities, and other unique needs and can’t rely on taxis or ride-sharing services

Driving is a right of passage for younger people to expand their boundaries from home, community and city

What do you think? Stakeholder changes are a big topic in any industry, particularly in self-driving. What are your thoughts?

OATV, or O’Reilly AlphaTech Ventures, is a seed stage investment firm based in San Francisco with a track record of backing robotics startups in emerging areas. As well as investing in Fetch Robotics, some of their other hardware investments include 3D Robotics, Planet Labs, Misfit Wearables, Littlebits and Sight Machine. OATV typically invest between $250,000 and $2 million into startups at a critical early stage of development. This pre-revenue runway helps startups refine their prototypes, determine product/market fit, and achieve strong follow on rounds. OATV invests early, typically before market categories are well defined.

Interview with former OATV Principal Roger Chen

Edited for clarity

What’s OATV’s investment thesis and how does that make you look at robotics companies?

Roger Chen, former OATV Principal

We like to look on the edge. If you take a look at our portfolio, there’s a wide array of companies in different categories. You have anything from consumer internet companies like Foursquare to satellite companies like Planet Labs to drone companies like 3D Robotics and logistics companies like Fetch Robotics. We made each investment when we sensed the emergence of a new category. When we think a “thing” is going to become a “thing,” we try to find companies and entrepreneurs in those categories very early on and back them just before the categories are really created. Before 3D Robotics, drones wasn’t really much of a category. And neither was space before Planet Labs and other pioneering companies like SkyBox.

Our focus has been on that strategy applied at the seed stage. We’re a little bit different than other seed firms in that we invest in fewer companies, about six a year. We concentrate more capital into those companies and take more of an all-in approach. Our personal philosophy and style is to try to work more closely with the companies we invest in, and it becomes hard and unwieldy to do that if you invest in too many companies within one year.

When it comes to robotics, we are seeing a lot of interesting things happen. There has been a confluence of technologies enabling new forms of robotics, from innovations in actuators enabling compliance and collaborative robotics to innovations in sensors and software.

ROS, or Robot Operating System, only emerged these last few years, and before that, software development for robotics was exceedingly difficult. The advent of open source communities and platforms like ROS has really catalyzed the field. So those are some of the enablers on the technology side.

There’s also a lot happening on the market side, and market pull is just as important as technology. Just to give one example, let’s take a look at e-commerce and what’s happening with consumers. They want things faster, cheaper, and personalized, and this just creates so much pressure on a lot of these manufacturing, supply chain, and logistics companies.

At the same time, there are macro trends within the labor economy, as baby boomers start getting older and labor supply is expected to drop significantly. The confluence of all these factors puts logistics companies in a tough spot. People tend to forget that someone somewhere still needs to make, package, and ship things as part of e-commerce’s backend. Suddenly, automation and robots make a lot of sense and are economical.

That’s how we see the robotics industry, and while that example is specific to the logistics industry, I think there are a lot of industries where automation and robotics are going to come into play in similar ways. It’s going to be a collision between technology enablers on one side and intense emerging market demand on the other.

Could you expand on some of the trends enabling robotics and automation in logistics?

I’ll talk a little more about market pull. Depending on country, online sales make up somewhere around 10% of overall retail. You can see how massive companies like Amazon and Alibaba are, and that 10% online share of retail will only continue to grow. It speaks to the growing volume of work that has to be fulfilled on the backend of e-commerce.

I think a lot of people, especially consumers, don’t see how much work has to go into fulfilling those online orders. There is a box that has to be moved. There is something that has to be packed. There is something that has to shipped and transported. That’s kind of shielded away from consumers’ eyes. But it all has to be done, and it’s becoming more and more challenging for logistics companies to fulfill all these operations economically.

I can give you another statistic on the labor side. A lot of people have concerns about how robotics and automation will disrupt labor, which I think is valid and true to a certain extent. But I think you also have to be nuanced about it because if you actually look at the manufacturing and materials handling industry, particularly in the US, there is a huge job gap of 600,000 people because there is not enough sufficiently skilled labor to execute on the work to be done. That then presents an opportunity for robotics and automation to come in and fill that gap.

These are the powerful forces we see driving robotics: the really intense demand for logistics fulfillment, and simultaneously a lack of people to do all the work at an economical cost.

What other areas of the commerce value chain can robotics, smart automation and AI potentially improve?

There’s a ton of room for cost reduction via automation, but it’s not necessarily with just physical automation. There are software solutions as well that can make supply chains a lot more productive. For example, our portfolio company Fetch Robotics is tackling the logistics problem by streamlining operations in factories and warehouses with a mobile robotics platform. However, Fetch will be just as much about its future operations management software and application data as its material handling robots.

At some point, all the goods that a company like Fetch moves around will need to be packaged into containers to be shipped all around the world. Another OATV company called Haven is creating a marketplace for streamlining how container shipping is booked. If you think about it, it’s rather ridiculous that people still have to call one another and use manual paper-based processes to mix and match which containers should go on which ship. It’s just very inefficient, and it hurts business by not maximizing fulfillment of shipping capacity. This is a case where relatively simple automation through purely software and a web application can go a very long way in driving up productivity in the supply chain.

The take home message here is that when I think about automation for improving supply chains, it’s not necessarily just robots with arms that move around and pick things up. It’s as much about the software as it is about the hardware.

What are some examples of OATV portfolio companies, perhaps not robotics companies but where the lessons can be applied to robotics?

I just talked about Haven a little bit – it’s essentially an online marketplace for more efficiently filling capacity on ships for shipping things.

There are a couple other OATV companies that come to mind. One is Sight Machine. It’s

a data platform company. They aggregate data streams across the manufacturing floor, perform analytics on them, and offer a frontend dashboard for customers to understand exactly what’s happening along their manufacturing lines. That has a ton of value because that kind of intelligence is what will allow decision makers overseeing operations to keep things up and running efficiently.

Another example is Riffyn. They are similar to Sight Machine in that they are also a data platform that aggregates data streams, but their focus is on the R&D lab for life science companies. Currently 70-90% of R&D results in the life sciences are not reproducible. If you are a pharma company, imagine the egregious amounts of R&D money wasted due to poor process control. Companies like Riffyn perform data automation to give science-driven enterprises control of their processes again. They automate data collection, root cause analysis and continuous deployment of improved process designs to drive up productivity for the R&D pipeline.

Both Sight Machine and Riffyn automate workflows to enable superior operational intelligence, flexibility, and performance to drive up productivity. While neither company is a robotics company in the traditional sense, that exact value proposition very much applies to robotics as well.

How is robotics today different from robotics in the past?

Once upon a time, robotics was about stationary, highly repetitive, high performance, and generally expensive automation. Industrial robot arms would repeat the same action again and again with extreme precision. We’re not as excited about those applications. We think a lot more about flexible robotics. We think about programmable robotics.

It’s no longer just about robotics automating specific human tasks. It’s more about how flexible robotics will enable superior operations overall. I would actually draw a parallel with what’s happening in the software world with the DevOps movement, which I think we’re shortly going to see in the physical world. With DevOps, the idea is to leverage a closed feedback loop to quickly iterate on software development, deployment and operations in a continuous fashion. I think this concept of continuous development and deployment will extend beyond virtual environments to optimize physical operations as well.

Companies like Fetch Robotics have a physical hardware platform that automates some process, which it will do well, but probably not perfectly at first. However, it will continuously improve and learn about the process because of all the operational data and analytics that result from prior deployments. That data will come back to decision makers and engineers and inform them how to redesign and improve process. Now, imagine a simple firmware or a software push that instantly reorganizes and improves operations

That’s the sort of robotics we’re seeing these days, and I think that’s what makes these companies really exciting. Robots are no longer one-trick ponies that just automate a single task.

Do you think these trends are leading to a change in the business model away from robots as capital expenditure? Will we see robots as a service? Or robots as a delivery mechanism for sensors and analytics?

At the end of the day, the decision to use robotics is still at its core a question of ROI. For some companies the ROI math doesn’t add up, but for an increasing number of companies, I think it does.

I do think though that there will be some interesting and innovative business models for robotics. How will future robotics products be priced? Some companies will make money selling hardware like more traditional industrial robotics companies. A company like Fetch Robotics makes a physical product that it will sell, but at the same time, there are potential SaaS-like revenue streams through the data applications and operations software that the company will offer. I’m definitely excited to see what new business models come out of all this.

And in conclusion?

I’m excited about this new wave of robotics companies evolving from traditional robotics that have primarily been about static, repetitive processes. We are witnessing the emergence of the first platforms to offer flexible and programmable robotics that we haven’t seen before.

I’m also really excited about learning what other verticals robotics will address. Most of the conversation about robotics has been centered on logistics and e-commerce, but there will be several other verticals as well. Applications like exploration, search and rescue, caregiving and more. I can’t wait.

The rest of our free report is available here — or in installments at Silicon Valley Robotics — featuring case studies and analysis from industry experts and investors.

If you enjoyed reading this post, you may also like..

Artificial intelligence that programs itself on the fly - from the team that developed Siri at SRI and Apple - was demonstrated this week in New York and it quickly performed complex spoken tasks, live and onstage.

At the recent TechCrunch Disrupt event, held in New York City May 9-11, Dag Kittlaus unveiled Viv, the new single-source cross-platform voice assistant for the thousands of apps available to us. Viv describes itself as an AI platform that enables developers to distribute their products through an intelligent, conversational interface. Kittlaus expects to offer Viv SDKs to developers in the fall and hopes to fully launch by the end of 2016.

In the video below of his 14-minute presentation and demo, with another 10 minutes of Q&A afterwards, one can easily imagine how Viv will soon become integral to the way we use and operate our apps. Viv provides a paradigm shift in the way we effect our daily tasks -- the very shift that others are attempting to provide in the form of personal assistants. It is a breakthrough accomplishment in providing a single conversational user interface (UI) to recognize our words, determine our intent, and then write code to effect that intent. As a side benefit, the video is very informative about the process of AI. [Forward to 4:00 and watch for 10 minutes just to see the demos and skip the intro and Q&A.]

Jibo, Pepper, Alexa, Duer, Cortana, Google, Watson and many others (startups are popping up every few days) are all in various stages of presenting and bringing to market their versions of personal assistants - some physical, others virtual.

But the Viv demo - done live - was speedier than any and Kittlaus explained why: because as more and more apps become available, and as more and more users want to use some of those apps, a personal assistant must scale to handle all those functions and the larger the scale, the more complex it becomes, the more lines of code that must be written, and it ultimately will slow down. Conversely Viv has a dynamic program generator that writes solution-based code from the intent of the user. In other words, Viv's AI parses through the words you say to determine intent and then writes only the software that meets the specific task requested and does it quickly. The video also shows, but doesn't detail, how Viv determines intent (goals) from the words. It breaks down the conversation into goals and values within thereby instructing the dynamic program generator which apps are required and what the parameters are for those apps.

Is Viv going to eliminate Google as the middleman? Kittlaus says that search isn't going anywhere but as Viv and other new AI assistants become more capable and become the primary resource for users, people really won't want to go back to the old way.

Siri, co-founded by SRI's Dag Kittlaus and Adam Cheyer and by Tom Gruber, was spun-out from the SRI International Artificial Intelligence Center and acquired by Apple for $200 million in 2010. Kittlaus left Apple in 2011; Cheyer left in 2012.

BOTTOM LINE

Personal assistants are all about simplifying the process of performing daily tasks. They are attempting to be what you would expect of a knowledgeable executive assistant working alongside to maximize your productivity and minimize your involvement, a person who really knows you and doesn't need you to reexplain things over and over. The list of vendors is impressive: Amazon, Google, Facebook, IBM, Baidu, Microsoft, Apple, SoftBank, all the car companies, many large consumer product providers and smaller companies like Jibo. To date, none have achieved that sweet spot where end users are fully satisfied.

The holdup has been the software, the need for extensive coding, and the ability to identify "intent" from sounds recognized as words. The breakthrough technology that Viv is offering is a way to change the way programmers work with computers and developers offer their products. Programmers will no longer have to instruct step-by-step procedures in rigid code, but instead they'll just have to describe the process and intent and the AI will develop the code - it will write the programs needed on the fly. And developers will just need to add Viv as their conversational UI.

Lockheed Martin CTO Keoki Jackson ’89, SM ’92, ScD ’97 (center, left) and MIT AeroAstro department head Jaime Peraire congratulate each other after signing a research collaboration agreement between the two organizations. Initial research will focus on robotics and autonomous systems. Photo: William Litant/MIT AeroAstro

In a new collaborative initiative in autonomy and robotics, MIT and Lockheed Martin scientists will focus on innovations needed to enable generation-after-next autonomous systems. Improvements in human/machine teaming and navigation in complex environments are among the research challenges that Lockheed Martin is inviting MIT faculty and their students to help solve.

“We have a valued relationship with MIT and are looking forward to moving to this next chapter and partnering with world-class researchers,” said Keoki Jackson ’89, SM ’92, ScD ’97, Lockheed Martin’s chief technology officer. “We are focused on advancing technology and recruiting top talent, both of which are crucial for creating the next generation of aerospace systems.”

A master agreement between MIT and Lockheed Martin, led by the Institute’s Department of Aeronautics and Astronautics (AeroAstro), and in collaboration with MIT’s Computer Science and Artificial Intelligence Laboratory, was formalized May 13 at a signing ceremony on campus. It provides a multiyear framework between MIT and Lockheed Martin for collaborative research, exchange of visiting scientists, support of student undergraduate research opportunities, fellowships, and internships at Lockheed Martin.

“We’re making the investment today, not just in research and development of the technologies that could have the most impact on future generations, but in the talent of these amazing individuals that will truly shape the future,” said Padraig Moloney ’00, Lockheed Martin program manager and architect of the new initiative. “We’re confident that our relationship and collaboration in these technical areas will influence the fields of autonomy and robotics for the next 15-20 years.”

AeroAstro department head Jaime Peraire said, “We’re delighted with this new agreement, which furthers a relationship between MIT AeroAstro and Lockheed Martin that goes back many years. It formalizes our partnership, and aligns with MIT’s mode of conducting research and education by melding academic rigor with real engineering challenges and applications.”

Initial research will be conducted by AeroAstro professors Jonathan How, Nick Roy, Sertac Karaman, Julie Shah, and Russ Tedrake and Department of Mechanical Engineering Professor Sangbae Kim.

In China's relentless state-stimulated quest to grow their robotics industry, Midea Group, a Chinese appliance manufacturer which already owns 13.5% of KUKA's shares, has offered to buy all remaining shares at a 59.6% premium thereby valuing the sale price at $5.2 billion.

KUKA AG, an Augsburg, Germany-based manufacturer of robots and automated manufacturing systems, is one of the Big Four in worldwide robotics sales along with Yaskawa Electric, FANUC and ABB. KUKA also owns Swisslog, a provider of robotics and automation solutions for hospitals, warehouses and distribution centers. Kuka has had a growing presence in China including a new factory in Shanghai in 2013.

Midea Group is a China-based manufacturer of household electronics including air conditioners, refrigerators and washing machines.

“Midea wants to build smart factories that use less labor to produce smart appliances, as China’s working population is dropping and they need to adjust to higher labor costs,” said Juliette Liu, an analyst at Yuanta Securities Co. “The company intends to use Kuka to establish a dominance over industrial robotic manufacturing techniques in China.”

Midea has been on an acquisition spree with a cash fund purported to be over $10 billion. Earlier this year Midea acquired an 80% interest in Toshiba's home appliance business for around $475 million and established an e-commerce unit for an undisclosed amount.

Henrik Christensen, KUKA Chair of Robotics at Georgia Tech, said:

China wants to become a major player in robotics and by acquiring KUKA they move from a fast follower to being a leader. It is impossible to buy ABB or FANUC, but KUKA is small enough that it is “easy” to do a take over. I suspect they may have to up the offer a bit, but I see it as a foregone conclusion.

Robotics today is a fast growing industry with applications in myriad markets, including retail, transportation, manufacturing, and even as personal assistants. Fellow Robots is at the forefront of reimagining these uses for the best retail experience – to improve your experience when shopping and to help employees with the most up to date product information and location of goods and services.

Fellow Robots is a multidisciplinary young team from different backgrounds, ranging from robotic, software wizards and data scientists to designers and business experts. We have built many platforms including telepresence robots, humanoid robots, sensors, cloud computing and more cutting edge technology platforms. We came out of SU Labs at Singularity University at NASA Research Park in Silicon Valley. SU Labs connects corporate innovation teams with startups and other organizations to explore exponentially accelerating technologies and create new sustainable business solutions. What distinguishes Fellow Robots is the ability to partner and work shoulder to shoulder with customers to learn how robotics can improve their retail needs.

Interview with Marco Mascorro, CEO and Co-Founder, Fellow Robots edited for clarity

Source: Silicon Valley Robotics

I’m Marco Mascorro, CEO and co-founder of Fellow Robots. Fellow Robots came out of Singularity University. Singularity University focuses on exponential technologies, with robotics being one of them. We started with a team of very passionate robotics engineers looking into industries that have not changed a great deal. We quickly honed in on the retail industry; specifically offline retail. For all the accomplishments of ecommerce and online retail in recent decades, about 90% of retail purchases still take place in store. This is clearly an industry overdue for a big step into technology, and we saw that robotics could be a great fit there.

We began by meeting with retailers and listening to them discuss the problems they are facing today, and have probably been facing for a long time. One of those early conversations was with Lowe’s. That conversation very quickly led us down the path toward a customer service robot.

I think that was a really interesting way to hear our customers, to see what kind of problems they were facing and how robotics technology could fit. Today, we have a partnership with Lowe’s to launch OSHbot, which is a customer service robot that helps customers find things in the stores. When the robot is navigating in the store, it knows where all the products are located. When a customer comes into the store they can just talk to the robot, in multiple languages. We can add up to twenty-five languages right now. We have English and Spanish working in the Orchard Supply Hardware store, owned by Lowe’s.

When a customer comes in and says, “Hey, I’m looking for nails and paint” then the robot can tell that customer where to find those items. It shows customers that it understands what is said. It displays on-screen the products that the store has in stock. It has a touch screen so customers can just navigate on the screen and see the pictures of the products and then click on the one that they actually want to see. OSHbot then tells the customer that the product is located in Aisle 15, for example, whether it’s in stock and some more information about the item. Customers can click on a button and follow OSHbot to the location of the item in the store.

The robot actually guides customers by its own fully autonomous navigation to the product location. Meanwhile customers are following OSHbot, there’s a screen on the back and that’s for engagement. It’s not very often we see robots talking to humans on a daily basis but I think that we are starting to see that now, and Fellow Robots and our customers are pretty happy about that.

The robot takes you to the product and then it gives you some extra options. If someone is buying paint, then it’s pretty common that they will also buy a brush. OSHbot can provide that information, and take the customer to the brushes as well. It’s a really interesting experience that the customer has now. It’s a whole new experience. Customers are going to stores and getting really accurate information about products, about what is in stock and where to find it.

If customers don’t want to follow the robot, OSHbot can just show them the product location on the map. The customer can decide to go on their own. One of the most interesting things we’ve seen so far is how quickly the adoption of new technologies is happening right now. Of course when we launched the robot in November last year, there was a “wow” factor. “But today if you go into the store it’s become so common, there’s no more “wow.” And we’re exactly seeing that path with OSHbot, as we saw with the smartphone industry.

So far you’ve described really successful interactions with OSHbot? Have there been difficulties?

There were a lot of unknowns when we first launched OSHbot, because hardly anyone has done this before. This is a customer service robot that’s actually working in the front of the store, helping customers and guiding them to specific locations. It’s very complicated to know how a robot is going to interact with people in stores, and how people and workers will respond to that robot.

Our primary realization was that customers interact with the robot almost exactly the same way that they interact with humans. The questions asked of OSHbot were questions they would ask a person.In the first month of deployment, we had someone right next to the robot collecting feedback, seeing how people interacted with the robot and where we could improve. That person was there taking notes on how customers were acting around and interaction with OSHbot.

Source: Fellow Robots

What’s complicated is that people ask questions in very different ways. So if someone says “Hi OSHbot, I’m looking for a quarter inch screw for my door.” The robot needs to be intelligent enough to know what product they are looking for: Is it the door? Is it the screw? So speech recognition was one of the things we needed to improve on, and we have. To make the interaction with the customer as smooth as possible we focus a great deal on natural language processing,

Another priority is our focus on is the customer interface. When you open an app, for example, you need to understand what the app does and how naturally to proceed to the next step. We have a very similar challenge with the robot UI. That’s why we have people on the Fellow Robots team whose sole focus is on the screen Interface and these interactions. How many clicks? Are they clear? Are they sufficient? Too many?

We have come to realize that what’s best is a combination of speech and screen interface. When the screen shows off the product, the robot tells you at the same time, “Here are the products available, click on the one you’re looking for.” People know what to do, and when they click on the product, they can choose to get taken there. So you provide a full interaction with the customer, where there is some speech and some visual interaction. Those were the big lessons learned from the first month of working with OSHbot in the store.

Will you be adding a product scanner to the OSHbot experience?

We have some of the things working along these lines but haven’t deployed them in the store just yet. One of the reasons is that there are a lot of factors not under our control. For example, we need to have a full 3D database of the products to be able to match those scans. That’s one of the reasons we decided to wait a little bit to deploy that functionality.

Probably about 20 or 30% of people that come to hardware stores have an object with them that they’d like to buy or that they have a question about. When a customer has a very specific question that the robot can’t answer, like “My pipe broke. What should I use to fix it? or “What glue should I use?” we have a store representative available at any time for that customer.

We added a small button on the screen that says, “Talk to an expert.” If a customer has a complicated question then the robot will tell you to click on that button and it connects you remotely to a store associate. That store associate can be located somewhere else, just as in a normal telepresence video conference call. That person can also be an expert in plumbing, in electricity, or any other field. This way the customer gets the ideal mix of automation and high touch service that retailers typically struggle with. That’s actually what’s happening right now.

So customers can have a mixed physical and virtual shopping experience?

Exactly. They could be talking to someone who’s an expert in paint, or electricity, or design, depending on what they need. This enables a really interesting way of interacting with store associates that’s very valuable.

What is the staff response to OSHbot?

It’s been really positive so far. I think one of the most interesting things we’ve seen is how fast OSHbot’s colleagues got used to working alongside a robot. I think we’re lucky that everyone had a very positive response. People like it, people use it.

How many OSHbots are in stores so far?

We currently have two robots located at the OSH in San Jose, CA. What is involved logistically in rolling out the robots? Are you getting close to rolling out more OSHbots?

We need to integrate the robots with the product database, but one of the nice things is that the robots have everything built in, so we don’t need to add any major additional infrastructure or sensors in the store to make the robot operate and navigate.

We are in conversations with customers about rolling out robots elsewhere.

How does OSHbot map the store and identify product locations?

Without going into too much detail, we can say that mapping is one of the robot’s core functionalities. The robot knows precisely where it is located at all times. We integrate that with the planogram, so this way OSHbot knows exactly where these objects are located on the shelves.

What other retail experiences would OSHbot apply to?

At the moment, our primary focus is in-store retail, but what’s key here is the level of premium customer service that the robot can provide. A robot can maintain accurate information of about 100,000 different products or more.

I think this capability can apply to different industries that also require customer service. When we talk to retailers, customer service is one of the biggest challenges, and one of the biggest opportunities. Therefore customer service functionality in the robot is vital, as is the speech recognition and the human interaction—to make it as natural as possible to provide a really nice experience. So in the future you see robots greeting people when they walk into bricks and mortar shops?

That’s the plan. The idea is to rethink how retail is done in terms of customer service and the experience you actually have when you go and purchase items in a store. You normally come with the idea that you’re going to buy a product, but you often ending up buying more. We want to help businesses make the process as smooth as possible, so that their customers find everything they need, everything they’re looking for, and have a great experience. That scenario is a win/win for both the retailer and the customer.

That’s a clear value proposition for the front of store. Does it extend into the back of store – doing inventory etc.?

There’s lots of potential there. For example, when the robot navigates the store it creates a map in order to know where products are located. But if a store associate moves products from one location to another, it’s challenging to inform everyone in the store. The robot can then can provide that information to the store associates.

So OSHbot will be providing customer service to the associates too?

Yes, right now we’re talking about how we can make this experience even richer for employees.

We feel that we’re at the very beginning of a trend where robots are gaining traction with industries that haven’t traditionally looked to robotics.