NTT’s recent entry into consumer robotics suggests that it’s not just about Google vs Amazon, or Softbank vs NTT anymore, but about telcos vs big data companies. With two major and distinct sectors now competing for market share in consumer robotics, will this impact the way the whole robotics industry evolves?

In the winter of 2013/14 major league US-based big data companies like Google, Apple and Amazon propelled robotics into mainstream news when they started buying and investing in robotics companies like Boston Dynamics, Kiva and Nest. The world was wondering: why do all these consumer-focused big data companies suddenly care so much about robots? Now it seems that the big data sector is not the only one with its eye on robotics. This spring Japanese telecommunications firm Softbank acquired Aldebaran’s Pepper robot, and just yesterday, the competing and much larger Japanese telco NTT announced it would be partnering with consumer robot manufacturer Vstock to offer its Sota robot to consumers on a subscription basis.

Is this a signal that the telecommunication sector will become just as interested in robotics as big data companies are?

The two Japanese telcos will be leveraging their robotic acquisitions/partnerships to market their core business – communications services like networking, broadband and data delivery – to their massive existing consumer base. For telcos, this seems a logical extension of the cell phone business model: the device itself is a loss leader and the revenue earned is in the subscription fees. Softbank will be charging about $1600USD plus a $30USD subscription fee for the consumer model of Pepper, and about $440USD/month for the recently announced enterprise model. NTT will be charging about $800USD with a monthly service fee of about $30USD for Sota.

These rates are far higher than a smartphone, and so it remains to be seen whether customers can see added value in the service over existing ones. Success may hinge on first developing niche markets, for example healthcare. Indeed NTT says it will roll out Sota as a companion robot in seniors homes next March, and Softbank’s first corporate customer is Nestle, who will be soon be launching Pepper as a marketing and service assistant in its Nescafe stores.

It remains to be seen whether, when, and how far telcos in other countries will latch on to the same trend. Softbank and NTT are located in Japan, whose population has a general love and affection for robots, and has traditionally had a strong consumer support for technology. The government of South Korea is active in marketing robotics to its people (they are even building a giant theme park dedicated to promoting robot tourism) and also seems like a good candidate. South Korea’s two top telcos, SK Telecom and KT, have both launched consumer robots. About taking Kibot into global markets, Seo Yu-Yeol, president in charge of KT’s Home Business Group has said: “We continue to conduct market surveys on each country’s network infrastructure such as broadband and WiFi services.”

There are surely others.

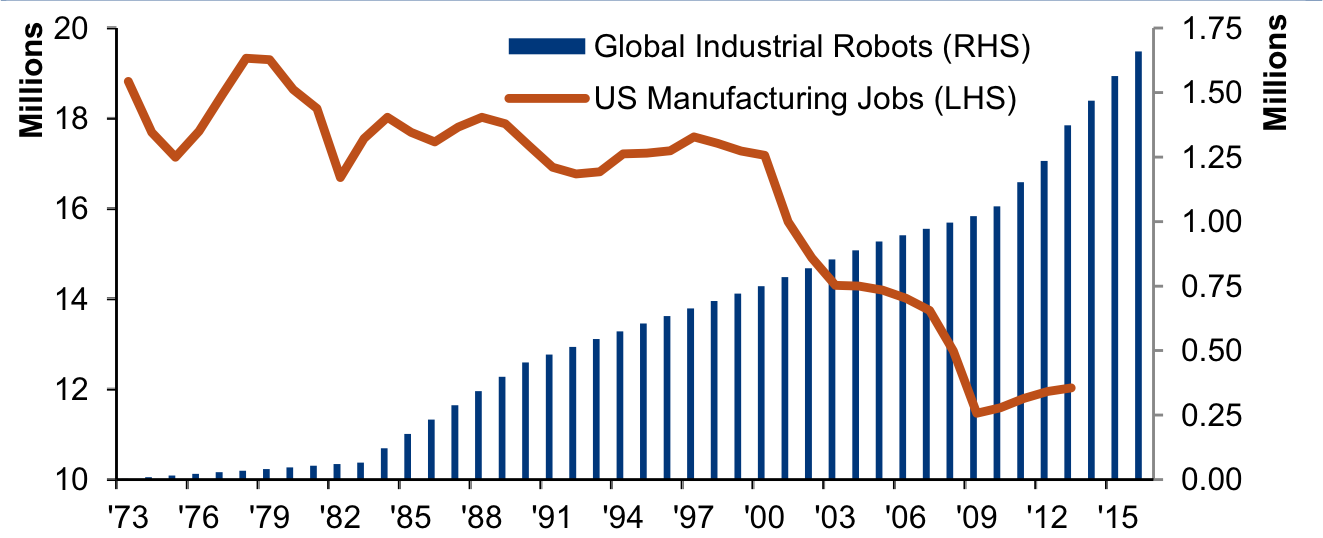

But returning to the original question of telcos vs big data companies … is it a stretch to say this is a game changer? Compare the fledgling consumer robotics industry to the early auto industry, where the oil, gas and electricity sectors all fought for influence. The oil sector largely won out and we have the gasoline-powered car; and it’s no coincidence that Elon Musk is invested in both electric cars and solar power … Through the eyes of the energy producers, the car is just a delivery vehicle for energy consumption.

Or perhaps it’s not telcos vs big data companies at all, but rather telcos AND big data companies. As evidenced by the Uber and Airbnb, the continuum between carrier, medium, data and service is getting blurrier by the day.

Either way, with these sectors driving the next wave of the consumer robot economy, how will this shape how we use, interact with and consume robotics technology? To paraphrase Frank Tobe in his recent Robot Report newsletter, it could be that: “We are watching robotics turn from industry to ubiquity before our eyes.”

Following an in-depth discussion on the topic at Robohub’s editorial meeting today, it seems at this point there are many more questions than answers …

- Is this even a game changer? or is it just hype?

- Which sector – big data or telco – is better positioned to capitalize on consumer robotics? Or will these sectors work together in partnership?

- Will we see a ‘dumbing down’ of social robotics systems as they become mass marketed consumer products? Or will the competition between telcos and big data inject energy and money into R&D ?

- How will niche markets, such as healthcare or service industry, impact the development of social robotics?

- Are there substantive differences between social robots vs. the other smart devices that telcos are currently using to deliver their services? Or in Noam Chomsky’s words: Is the medium the message?

- How will all this impact robotics research and development? Will it benefit or harm the robotics community?

- Will we see a regional consolidation of telco investment, for example in Japan? When will telcos from other countries jump into the market?

- How does telco involvement impact privacy issues?

- Will this help usher in robot-as-a-service (RaaS) as an accepted business model?

To explore these questions, and many others, Robohub will be renewing our focus series Big deals: What it means to have the giants investing in robotics (started back when the Googles and the Amazons were first getting into the fray) to explore how telcos might be changing the game.

Interested in joining the discussion? Leave a comment below or email us at info@robohub.org with your contribution ideas.

A special thanks to Robohub team members Andrea Keay (@robotlaunch), Sabine Hauert (@sabinehauert), Adriana Hamacher (@AdrianaHamacher), John Payne (@lacyiceplusheat) and Audrow Nash for their stimulating discussion and input.

If you liked this article, you may also be interested in:

- Japanese telcos vie for share in consumer robot-as-a-service business

- Softbank will take pre-orders for enterprise version of Pepper starting Oct 1

- Forget Google and unicorns, Asian dragons are going to dominate robotics

- Foxconn and Alibaba invest in SoftBank Robotics as Pepper goes on sale in Japan

- Nestlé 1st big buyer of Softbank’s Pepper robot

- Natural language: The de-facto interface convention for social robotics

- The second wave of social robots is here

See all the latest robotics news on Robohub, or sign up for our weekly newsletter.

Virtual Incision Corp.

Virtual Incision Corp.

[RG] We started Clearpath right out of university in 2009 as we finished our undergraduate degrees – I did my Masters at the same time as we were getting off the ground, which is generally regarded to be a bad idea in terms of stress levels. It’s hard to believe that we just celebrated our sixth anniversary this year.

[RG] We started Clearpath right out of university in 2009 as we finished our undergraduate degrees – I did my Masters at the same time as we were getting off the ground, which is generally regarded to be a bad idea in terms of stress levels. It’s hard to believe that we just celebrated our sixth anniversary this year.

Established in Berlin in 1847, and with a presence in Silicon Valley since the 1950s, Siemens invests more than $1B in the US each year for research and development. Now their Technology to Business team (TTB) has launched the Frontier Partner program, which aims to give startups in robotics and 3D printing a head start by providing them with software and resources to accelerate the development and manufacturing of their products. We spoke with Director of Strategy for Siemens PLM Software, Andy Swiecki, about why Siemens is focusing on robotics right now, and what startups can expect to get out of the Frontiers program.

Established in Berlin in 1847, and with a presence in Silicon Valley since the 1950s, Siemens invests more than $1B in the US each year for research and development. Now their Technology to Business team (TTB) has launched the Frontier Partner program, which aims to give startups in robotics and 3D printing a head start by providing them with software and resources to accelerate the development and manufacturing of their products. We spoke with Director of Strategy for Siemens PLM Software, Andy Swiecki, about why Siemens is focusing on robotics right now, and what startups can expect to get out of the Frontiers program.

At last week’s RoboBusiness Conference and Expo in San Jose, there was much gossip, discussion and head scratching regarding the two most recent acquisitions of robot companies: Adept Technologies by Omron and Universal Robots by Teradyne.

At last week’s RoboBusiness Conference and Expo in San Jose, there was much gossip, discussion and head scratching regarding the two most recent acquisitions of robot companies: Adept Technologies by Omron and Universal Robots by Teradyne.

Robots in Depth is a new video series featuring interviews with researchers, entrepreneurs, VC investors, and policy makers in robotics, hosted by Per Sjöborg.

Robots in Depth is a new video series featuring interviews with researchers, entrepreneurs, VC investors, and policy makers in robotics, hosted by Per Sjöborg.

CyPhy Works

CyPhy Works RightHand Robotics

RightHand Robotics

Bosch, the Germany-headquartered global conglomerate, began moving into their new

Bosch, the Germany-headquartered global conglomerate, began moving into their new  Robots in Depth is a new video series featuring interviews with researchers, entrepreneurs, VC investors, and policy makers in robotics, hosted by Per Sjöborg. In this interview, Valery Komissarova — Business Development Director at Grishin Robotics — talks about her work at an investment company focused on consumer robotics.

Robots in Depth is a new video series featuring interviews with researchers, entrepreneurs, VC investors, and policy makers in robotics, hosted by Per Sjöborg. In this interview, Valery Komissarova — Business Development Director at Grishin Robotics — talks about her work at an investment company focused on consumer robotics.

SZ DJI Innovations

SZ DJI Innovations The two new labs will be part of Toyota Research Institute and be headed by Gil Pratt who recently headed the DARPA Robotics Challenge. Toyota said that, in addition to autonomous driving, they plan to develop AI "technologies for everyday use, delivering a safer lifestyle overall." “This is the first small step that allows us to go beyond automobiles and make use of the Toyota group’s potential by utilizing artificial intelligence,” Toyota President Akio Toyoda.

The two new labs will be part of Toyota Research Institute and be headed by Gil Pratt who recently headed the DARPA Robotics Challenge. Toyota said that, in addition to autonomous driving, they plan to develop AI "technologies for everyday use, delivering a safer lifestyle overall." “This is the first small step that allows us to go beyond automobiles and make use of the Toyota group’s potential by utilizing artificial intelligence,” Toyota President Akio Toyoda. In another announcement last week from the

In another announcement last week from the

Robots are starting to move out of the factory and into more common use as a service industry, where they work alongside people in places that range from the warehouse to the supermarket. Along the way, we need to ask: How do we integrate robotics into society? And what roles can robots play? A new report released today by Silicon Valley Robotics and titled “

Robots are starting to move out of the factory and into more common use as a service industry, where they work alongside people in places that range from the warehouse to the supermarket. Along the way, we need to ask: How do we integrate robotics into society? And what roles can robots play? A new report released today by Silicon Valley Robotics and titled “